How to save for retirement as a freelancer

Saving for retirement as a freelancer or self-employed isn't always easy—but it is important. 3 experts share tips for creating your plan.

share this article

Ready to find freelancing opportunities?

According to the Freelance Forward 2022 survey, 39% of Americans now freelance either full-time or as a side hustle. One of the popular reasons they cite for freelancing is “to be in control of my financial future,” yet for many contractors, saving for retirement remains a question mark.

Consultant and We Are Rosie community member Jeff Sugarman found himself reconfiguring his retirement plan after losing his corporate job due to downsizing. Over three decades, Jeff rose through the ranks from graphic designer to creative director at Staples. His severance package enabled him to springboard into self-employment and fulfill a dream by launching Ora, a brand strategy and design firm.

“My wife and I had retirement plans in place already,” he explains. “Our [financial] advisor helped us modify it to meet my changed income. Neither of us is particularly focused on money, so it’s good to have someone who can provide us with objective advice.”

Retirement looming in the not-too-distant future forced Jeff to learn how to prioritize and meet his retirement goals. To help other consultants fill this knowledge gap, we spoke to experts to get their take on the best ways to save for retirement as a freelancer.

Secure your financial future: 5 expert tips for retirement planning for freelancers

Taking the first step is often the hardest part. We asked an independent marketer, a CPA, and a financial advisor to share their perspectives and approaches to retirement planning for freelancers.

1. Master the financial basics

Self-employment comes with a unique set of financial challenges. Managing cash flow, finding health insurance, and paying self-employment taxes are just a few hurdles freelancers need to tackle without any training. All of these financial practices are interconnected, though. It’s impossible to succeed at retirement planning unless you’re working toward healthy financial habits in your business and your personal life.

“I wish financial advice and business acumen had been part of my college education,” Jeff shares. “When I was in school, I didn’t realize that many designers end up as freelancers. It would have been helpful if schools pointed this out and prepared new designers for this eventuality. Learning the basics of running a small business should be part of every designer’s education.”

So, what financial basics should you work toward?

Create a budget

No matter your age or how long you’ve been freelancing, it’s important to start small to build some momentum and create good financial habits.

“For someone who isn’t currently saving, a good place to start is a budget,” says Seth Adamson, Financial Advisor at UBS. “I recommend using a website or app like Mint.com to start tracking your inflows and outflows. It can be a bit labor-intensive in the beginning, but you can link credit cards and bank accounts so that your spending is eventually automatically captured and categorized.”

Build savings

In addition to a budget, start building an emergency fund with at least three to six months’ worth of total spending set aside in a short-term “rainy day” fund. This can offset any ebbs and flows or gaps in your income.

It’s also important to learn the difference between saving and investing and where to use each strategy. For money you don’t need to access in the near future (like your retirement funds), investing is important. But because of the risk of market fluctuations, a high-yield savings or money market account is a better choice for your emergency fund. You won’t risk losing money but you’ll still get some return: a 5% yield on a $20,000 emergency fund is $1,000 in annual interest—that’s meaningful money that shouldn’t be left on the table.

Figure out self-employment taxes

“Freelancers need to make sure that they’re staying on top of their taxes,” advises Seth. “Without a pre-set salary or regular payroll tax withholdings, this can be challenging. A general rule of thumb is to set aside around 25% to 30% of before-tax income to cover quarterly estimated tax payments.”

Enrolling in a course like Know Your Worth by Amy Northard, CPA can help you learn how to manage your taxes and other topics like registering your business, bookkeeping, and small business deductions.

2. Get started as early as possible

The earlier you start saving for retirement, the better—don’t wait.

“The power of compounding works wonders, but only if you give it time to take effect. Your earnings eventually start to generate their own earnings!” says Seth. “Plus, long-lasting financial habits are often formed in these early years.”

3. Work with a financial advisor

“Having a financial advisor has been very helpful for my wife and me,” Jeff shares as he reflects on his transition from employee to consultant. His advisor helped adjust his wife’s 401(k) contributions and experiment with different IRA contribution amounts until they found the right amount for their lifestyle.

Since everyone’s situation is different, a financial advisor can assess your unique needs, recommend structures and investments to make the most of your dollars, and keep you within IRS rules and guidelines.

4. Network with other freelancers for tips and resources

Like many other areas of freelancing, one difficult aspect of saving for retirement is feeling like you’re on an island as an independent contractor. You can’t ask your HR department or a coworker—but you can learn from the vast community of freelancers out there through local meetups or online groups, including We Are Rosie’s community of independent marketers.

Hannah Baird, CPA and controller at We Are Rosie, advises that finding resources should be your first step to saving for retirement.

“A great way to do this is to ask other freelancers who are already saving for retirement who they use as their agent,” she says. “If you aren’t able to find anyone this way, do a search online for local retirement agents and browse their reviews.”

5. Automate your retirement savings

Independent marketers are great at using tools to automate parts of their business, and creating a system for retirement planning should be no different. “Make the funds move automatically from a checking/savings account into a retirement fund,” advises Jeff. “If you have to do it manually, it won’t happen.”

What are the options for self-employed retirement plans?

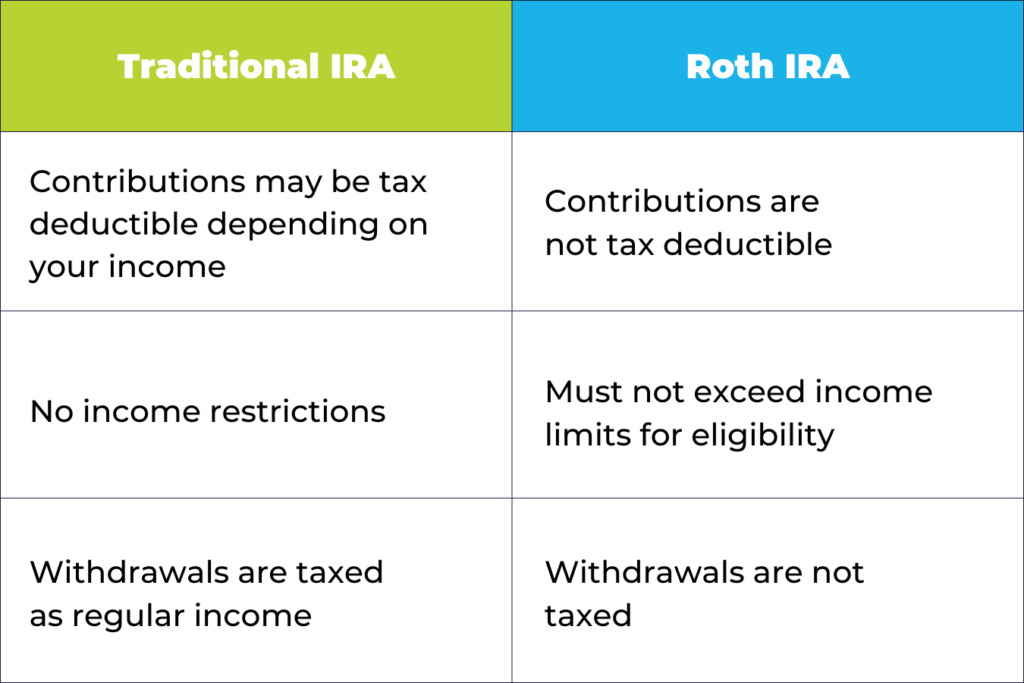

There are two primary ways to save retirement funds when you don’t have an employer-sponsored plan: a traditional IRA and a Roth IRA.

“With a traditional IRA, you contribute pre-tax dollars, meaning you’re taxed on the account’s growth when you withdraw money at age 59½ or later,” explains Hannah. “With a Roth IRA, you contribute after-tax dollars, meaning your money grows tax-free and you aren’t taxed when you withdraw money.”

With a traditional IRA, you’re able to get a tax deduction depending on how much you contribute. There’s no deduction for Roth contributions, but you’re limited in how much you can contribute annually, if at all, based on your income.

For those who aren’t in a high tax bracket, Seth suggests using a Roth IRA. And if you freelance through a community like We Are Rosie, you may have access to an employer-sponsored 401(k), too.

It’s important to note that many of these retirement accounts have income limitations, documentation requirements, and maximum annual contribution amounts, so seeking professional advice is crucial.

Is there such a thing as a self-employed 401(k)?

There is a self-employed 401(k) plan, called a Solo 401(k), which you can create for yourself if you’re self-employed with no employees. A Solo 401(k) has a higher contribution limit than a traditional or Roth IRA. Other options for freelancers include a SEP IRA or a SIMPLE IRA, both of which are designed for small businesses.

“For those who would like to save more than the traditional IRA and Roth IRA allow, it might be worth setting up a SEP IRA, SIMPLE IRA, or a Solo 401(k),” explains Seth. “These accounts can require some additional paperwork, administration, and fees, but can allow freelancers to save even more money for retirement.”

Is there a way to make up for the lack of an employer contribution?

If you’ve held a corporate job in the past, you likely miss that extra 5% (or however much your employer matched). Since you now are your employer, you need to think about ways to make that up.

The best way to do this is by making sure you’re charging enough and building the extra few percentage points into your fees. If you aren’t sure how to determine your rates, you can learn more in our 7 step guide to launching your career as a marketing consultant.

Additionally, the U.S. government is starting to recognize and support independent contractors’ needs with the new Saver’s Match program signed into law in 2023 through the SECURE 2.0 Act. Starting in 2027, the government will make a 50% matching contribution on up to $2,000 contributed to retirement accounts. So, for a freelancer who isn’t phased out due to income limitations, that could result in an annual retirement savings boost of up to $1,000.

How much should I save for retirement as a freelancer?

Hannah advises, “A common goal for saving for retirement is 20% of your income, but that’s not feasible for everyone. Even saving just a few dollars from each payment received makes a big difference [over time].”

Seth recommends a similar ratio, and suggests breaking down your after-tax income with the 50/30/20 rule: 50% on needs, 30% on wants, and 20% toward savings. However, the exact number isn’t as important as the mindset.

“Set long-term savings goals and make minor incremental increases over time to slowly work towards those goals,” he advises. “Especially as your income increases, get in the habit of automatically increasing your savings rates to coincide with any pay bumps. Otherwise, you’ll just get in the habit of spending more without even realizing it.”

Now that you know how retirement for freelancers works, don’t wait to start saving. You need a long-term outlook for retirement planning, so don’t get discouraged if you don’t see big results in the first few years. Set goals, find resources, consult a financial advisor, monitor your progress, and be sure to celebrate your achievements along the way!